A second child costs about 20% less per year than the first. But two children in daycare at the same time creates a financial crisis that derails more family plans than any other single expense.

Most parents who run the numbers on a second child start with the same assumption: the second one will be cheap. You already have the crib, the stroller, the clothes. How much more can it really cost?

The honest answer is: more than the gear math suggests, and less than you might fear — but the timing matters enormously. The difference between a second child being manageable and a second child being financially derailing comes down almost entirely to one variable: how long both children will be in paid childcare at the same time.

The 20% rule — and why it’s only half the story

Research from SmartAsset’s 2023 analysis of second and third child costs puts the average annual cost for a first child (ages 0-4) at $20,814. A second child the same age costs $17,413 — about 16% less per year. That’s a real saving, driven by a few categories that genuinely scale down:

- Health insurance: A second child adds no premium to an existing family plan. That’s roughly $3,000-$3,600/year that disappears from the marginal cost.

- Daycare sibling discounts: Most centers offer 10-20% off a second child’s tuition. On $17,000/year of infant care, that’s $1,700-$3,400 back per year.

- Gear and clothing: A crib that cost $400 with child one costs nothing with child two. Same for the stroller, high chair, and approximately 75% of the first two years of clothing if siblings are the same gender.

What the 20% figure doesn’t tell you is that the total family bill still rises by $250,000-$280,000 over 18 years. LendingTree’s April 2026 estimate puts the full cost of raising one child at $303,418. Two children cost roughly $520,000-$550,000 total. Per child, that’s about $260,000-$275,000 each — a 9-14% discount per child. Real, but not transformative.

What actually changes category by category

Housing

Housing is 29% of total child-rearing costs, per the USDA. It’s also the most variable factor for a second child. If your current home can accommodate two children sharing a room — which is common for families with children close in age — the marginal housing cost for a second child is zero. You’re already paying rent or a mortgage; adding one more person doesn’t change that.

If the second child pushes you from a two-bedroom to a three-bedroom, you’re paying a real premium — typically 10-20% more in rent or home price, not 50% more. Amortized across both children, the per-child housing cost still drops.

Food

Food costs roughly $3,377/year per child on average. A second child doesn’t double your food bill — it increases it by about 10-15%, primarily because bulk purchasing becomes more efficient and food waste decreases when quantities scale up. The increase becomes more noticeable in the teenage years when appetites peak.

Childcare

This is where the math gets genuinely difficult. Infant center-based care averages $17,264/year nationally, with a sibling discount of 10-20% for the second child. In high-cost states, those numbers scale dramatically:

| State | Annual infant care | Monthly |

|---|---|---|

| Massachusetts | $26,343 | $2,195 |

| California | $21,945 | $1,829 |

| Colorado | $21,840 | $1,820 |

| Texas | $10,706 | $892 |

| Mississippi | $6,868 | $572 |

A sibling discount of 15% in Massachusetts saves about $3,951/year. That’s meaningful — but you’re still paying $22,392/year for the second child’s infant care alone, on top of whatever your first child’s care costs.

Healthcare

This is the clearest win for a second child. If you’re already on a family health insurance plan, adding a second child adds exactly zero to your monthly premium. You still pay copays, prescription costs, and child-specific out-of-pocket expenses — roughly $1,688/year per child — but the premium line item disappears. That’s typically $3,000-$5,000/year in savings compared to what you’d pay for a standalone policy.

Activities and education

This is where the per-child savings stop. Sports leagues, music lessons, camps, and after-school programs are almost always priced per child. Families with two children often end up spending more in total on activities, even if they sometimes cut back on a per-child basis. Private school tuition, if applicable, is per-child — sibling discounts of 10-25% exist at some schools, but the base cost is still significant.

The real math: one child vs. two over 18 years

| One-child family | Two-child family | Per-child (two-child) | |

|---|---|---|---|

| Total 18-year cost | $303,418 | $520,000-$550,000 | $260,000-$275,000 |

| First 5 years (daycare) | $29,325/year | $46,500-$50,000/year | $23,250-$25,000/year |

| After school starts | $12,061/year | $21,000-$24,000/year | $10,500-$12,000/year |

| Per-child premium vs. two-child baseline | +27% | Baseline | Baseline |

The “only-child premium” in that last row is worth pausing on. The USDA data shows that raising one child costs 27% more per child than raising each child in a two-child family. This exists because fixed costs — housing, insurance, utilities — can’t be shared. A two-bedroom apartment that houses one child would house two. The insurance premium that covers one child on a family plan covers two. When those costs can’t be split, the per-child rate rises.

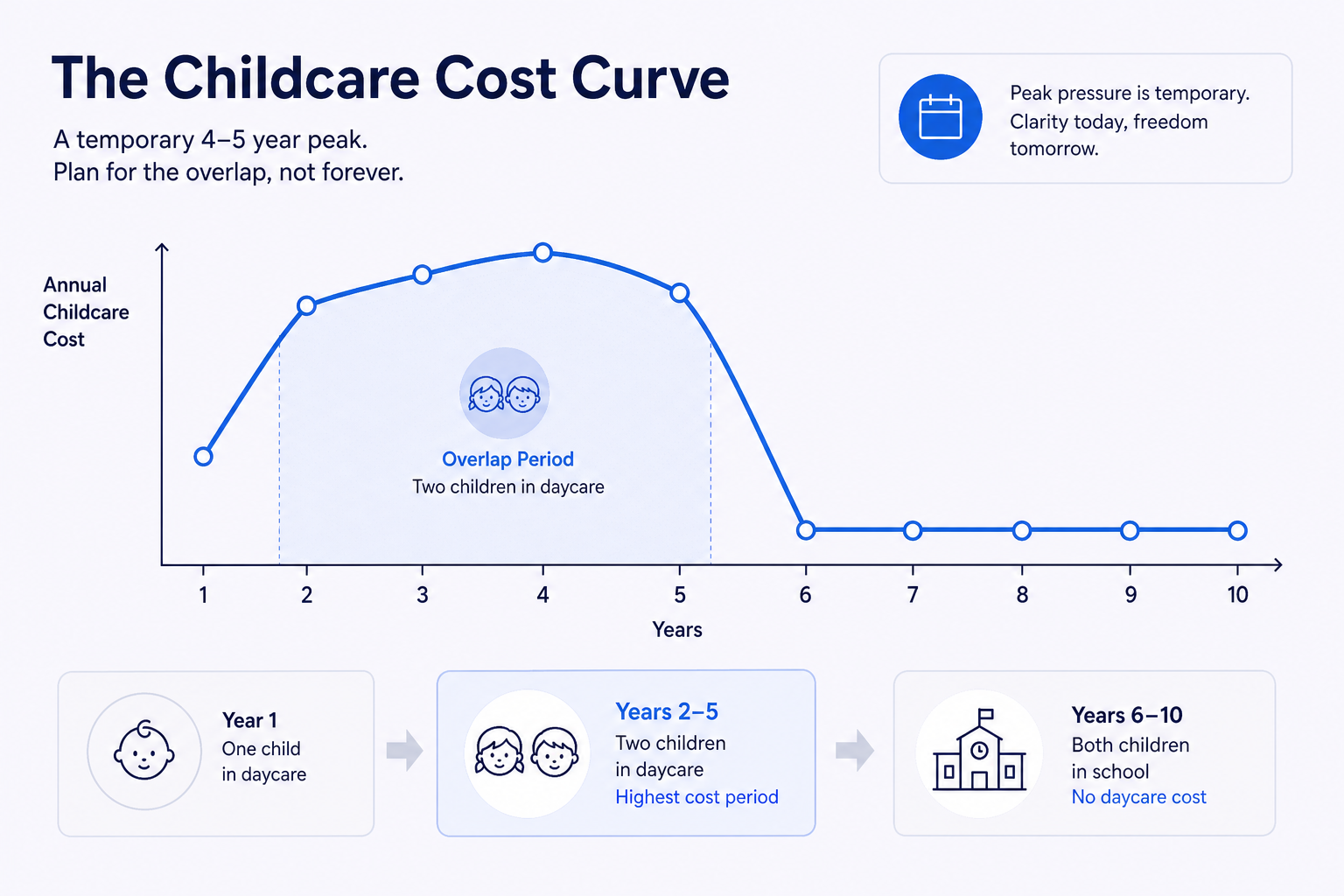

The simultaneous daycare problem

None of the above is what actually derails families. What derails families is this: a 4-5 year window when both children are in paid daycare at the same time.

“Living in eastern MA, two kids in daycare is $48k/yr total cost.” — r/personalfinance

“We can’t afford to have a second baby and I’m heartbroken. I can’t afford daycare for two and I can’t afford to quit my job to stay and take care of them.” — r/Mommit

The overlap window works like this: if your first child is born when you’re 30 and your second at 33, both children are in paid childcare from ages 0-3 (second child) and ages 3-6 (first child). That’s a 3-4 year stretch where both are consuming full-rate or near-full-rate daycare simultaneously. Once the older child enters kindergarten, the family’s childcare costs drop by 50%+ almost overnight.

The sibling discount softens this. Two children in daycare doesn’t cost double — it costs about 85-95% of double, depending on the center’s discount structure. But “85% of $34,000” is still $28,900/year, and in Massachusetts, it’s closer to $42,000-$45,000/year for two children simultaneously enrolled.

Three real scenarios

Scenario 1: Both parents working, national average daycare costs

| First child | Second child (marginal) | Change | |

|---|---|---|---|

| Daycare (with 15% sibling discount) | $17,264 | $14,674 | -$2,590 |

| Health insurance premium | $3,638 | $0 | -$3,638 |

| Clothing/gear | $800 | $200 | -$600 |

| Food | $3,377 | $3,715 | +$338 |

| Housing (no upgrade) | $5,440 | $0 | -$5,440 |

| Transportation | $2,814 | $2,533 | -$281 |

| Annual total | $33,333 | $21,122 | -$12,211 (37% less) |

Scenario 2: High-cost area (Massachusetts), both parents working

| First child | Second child | Change | |

|---|---|---|---|

| Daycare infant care | $26,343 | $22,391 | -$3,952 |

| Health insurance | $3,638 | $0 | -$3,638 |

| Clothing/gear | $800 | $200 | -$600 |

| Food | $4,208 | $4,629 | +$421 |

| Housing (no upgrade) | $6,892 | $0 | -$6,892 |

| Annual total | $41,881 | $27,220 | -$14,661 (35% less) |

Scenario 3: One parent works, one stays home (no daycare)

| First child | Second child | Change | |

|---|---|---|---|

| Daycare | $0 | $0 | — |

| Health insurance | $3,638 | $0 | -$3,638 |

| Clothing/gear | $800 | $200 | -$600 |

| Food | $3,377 | $3,715 | +$338 |

| Housing | $5,440 | $0 | -$5,440 |

| Activities | $1,200 | $1,200 | $0 |

| Annual total | $14,455 | $5,115 | -$9,340 (65% less) |

The stay-at-home scenario shows the largest savings because daycare — the biggest single line item in early childhood — is zero for both children. The second child costs $5,115/year in this model. That’s the floor.

The career cost most parents skip

Every budget comparison above is missing the single largest cost of a second child: its compounding impact on parental earnings.

U.S. Census Bureau research (2025) documents a roughly 5-10% wage penalty per child for mothers, and these penalties compound. A parent who takes extended leave, reduces hours, or exits the workforce for 2-3 years around a second birth may face a permanent wage baseline reduction. The first child already imposed a penalty; the second reinforces and extends it.

For a parent earning $70,000 at the time of a second child:

- 3 years of reduced career advancement: new baseline $59,500 (-15%)

- 5 years: new baseline $52,500 (-25%)

- These penalties don’t automatically reverse when children start school

Over a 20-year career, that wage differential can represent $200,000-$300,000 in lost earnings — far exceeding the direct childcare costs. It doesn’t show up in monthly budget comparisons, but it’s the most significant financial consequence of expanding a family.

“I am heartbroken that we can’t afford a second child. I would say we could wait 4 or 5 years but I’m already 39. We live in a HCOL area…” — r/Parenting

The timing problem is real. The biological window and the financial window don’t always align. Families who could afford a second child at 32 may not be in a position to at 37, and families who might afford it at 37 are up against different constraints.

What helps: tax credits and the real numbers

The federal tax treatment of children meaningfully reduces the net cost.

Child Tax Credit: $2,200 per child (2026). Two children = $4,400/year in direct tax reduction.

Dependent Care FSA: The 2026 limit is $7,500 per household — note this is per household, not per child. For a family paying $50,000/year in daycare for two children, the FSA covers the first $7,500 at pre-tax rates, saving roughly $1,650-$2,000 in federal and payroll taxes.

Child and Dependent Care Tax Credit: Covers 20-35% of up to $6,000 in expenses for two or more children. Can’t be claimed on the same dollars as the FSA — use the FSA first for better savings at higher income levels.

Combined, these reduce the net annual cost by roughly $5,000-$8,000 for families with two children in daycare, depending on income bracket and location.

When a second child is manageable vs. when it strains

Four situations where the math is more forgiving:

Large age gap between children (4+ years). If your first child is entering kindergarten when your second is born, the overlap window shrinks to zero. You pay full daycare for child two without also paying for child one — a materially different situation than two children in daycare simultaneously.

Low or moderate cost of living. A family in Mississippi paying $572/month for infant care faces a fundamentally different calculation than a family in Massachusetts paying $2,195/month. The second child’s marginal daycare cost is $486-$1,866/month depending on location — that’s the range of difficulty.

One parent stays home. With no daycare costs, the second child costs roughly $5,000-$8,000/year in marginal expenses. That’s a manageable increment for most households. The trade-off is the career penalty described above.

Flexible employment with genuine part-time options. A parent who can genuinely reduce to 60-70% of their hours (not theoretically, actually) during the overlap years can significantly reduce daycare needs without triggering the full career-stagnation effect.

Four situations where it genuinely strains a budget:

- Both parents working full-time in a high-cost city with no subsidy eligibility

- Ages close together (under 3 years apart) with both children needing full-time care simultaneously

- No employer child care benefits and ineligibility for state subsidies

- One parent already carrying a significant career penalty from the first child

“The cost of daycare per month is the same as my mortgage, and that’s on the lower end!” — r/Mommit

The only-child premium, revisited

One finding worth sitting with: raising one child costs 27% more per child than raising each child in a two-child family. The economies of scale are real. A parent who stops at one for financial reasons isn’t saving as much per child as they might expect — they’re paying a premium for fixed costs that can’t be shared.

This doesn’t make the decision simple. The career penalties are real. The simultaneous daycare window is real. The timing constraints are real. But the popular framing that “we can’t afford a second child because we’d have to buy everything again” gets the math backwards — buying-again is roughly 5-10% of the cost picture. Daycare is 40-50%.

ParentWorth

ParentWorth models the actual budget impact of family structure decisions, including the daycare cost comparison that underlies much of this calculation. The childcare cost guides by region cover state-by-state rates that change the math significantly depending on where you live.

Frequently Asked Questions

How much does a second child actually cost compared to the first?

A second child costs roughly 15-25% less per year than the first, according to SmartAsset’s 2023 analysis. In dollar terms for families with young children: first child averages $20,814/year, second child averages $17,413/year. The savings come from daycare sibling discounts (10-20% off), no additional health insurance premium on a family plan, hand-me-downs on gear and clothing, and amortized housing costs. However, total family spending still increases by $250,000-$280,000 over 18 years.

What is the total cost of raising two children to age 18?

Based on the LendingTree April 2026 estimate, one child costs approximately $303,418 to raise from birth to age 17. Two children cost roughly $520,000-$550,000 total — about $260,000-$275,000 per child. That’s a 9-14% per-child discount compared to raising a single child, driven by shared fixed costs like housing, insurance, and equipment.

Why is the simultaneous daycare period so financially difficult?

When two children are both in paid childcare — typically a 3-5 year window before the older child enters kindergarten — families pay 85-95% of the cost of two separate daycare slots. Even with sibling discounts, two children in infant or toddler care in a high-cost area can total $40,000-$50,000 per year. Parents in r/personalfinance commonly cite this period as the reason they couldn’t afford a second child, regardless of income level.

Does having only one child cost more per child than having two?

Yes — and by a surprising margin. The USDA found that raising one child costs 27% more per child than raising each child in a two-child family. The premium exists because fixed costs (housing, insurance, utilities) can’t be shared across multiple children, one-child families tend to spend more on enrichment and activities per child, and there are no sibling discounts on childcare. This is sometimes called the ‘only-child premium.’

What are the hidden costs of a second child that don’t show up in budget calculators?

The biggest hidden cost is the parental career penalty. U.S. Census Bureau research shows each child carries roughly a 5-10% wage penalty for mothers, and these penalties compound. A parent who reduces work hours or leaves the workforce for 2-3 years around a second child’s birth may see a permanent wage baseline reduction. Over 20 years, that lost earning potential can exceed $200,000 — far more than the direct cost of the child. Other hidden costs include pregnancy and birth expenses (~$18,865 average out-of-pocket), the complexity of managing two different schedules, and increased likelihood of needing backup care.